{kind=link}

{kind=link}

In the world of technology, there are moments when an emerging product category captures the imagination of investors, engineers, and governments alike—moments when a new platform promises not just incremental change, but a complete redefinition of how humans interact with machines.

The personal computer was one. The smartphone was another.

Now, a growing number of executives and analysts believe humanoid robots could be next.

Across Silicon Valley, Shenzhen, Tokyo, and Berlin, companies are pouring billions of dollars into the development of general-purpose humanoid robots—machines that can walk, talk, manipulate objects, and perform a wide range of tasks in human environments.

The stakes are enormous. Whoever succeeds in building a scalable, affordable humanoid robot platform could unlock a market worth trillions of dollars.

“This is the ultimate embodiment of AI,” said one venture capitalist. “If software was the first wave, and mobile was the second, humanoid robots could be the third.”

A Crowded and Fragmented Battlefield

The competitive landscape is already crowded.

On one side are established technology giants, leveraging their expertise in artificial intelligence, cloud computing, and hardware manufacturing. On the other are startups, moving quickly with focused strategies and bold engineering bets.

Some companies are pursuing vertically integrated models—designing everything from chips to software in-house. Others are building modular ecosystems, relying on partnerships for key components.

“There’s no consensus on the winning approach yet,” said a robotics industry analyst. “And that’s what makes this moment so volatile.”

At least four distinct strategies are emerging:

1. AI-First Approach

Companies in this camp treat humanoid robots primarily as a physical extension of artificial intelligence systems.

Their focus is on developing large-scale models capable of reasoning, perception, and generalization. Hardware, while important, is seen as a vessel for software intelligence.

2. Hardware-First Engineering

These firms prioritize mechanical design, focusing on balance, dexterity, and durability.

Their argument is simple: without reliable physical performance, even the most advanced AI is useless.

3. Platform Ecosystem Strategy

Some players aim to build an “operating system” for humanoid robots—creating a developer ecosystem similar to smartphones.

If successful, this approach could allow third-party developers to create applications, unlocking network effects and accelerating adoption.

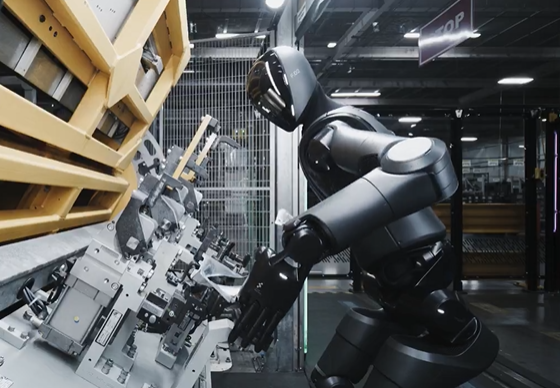

4. Industrial Deployment Focus

Rather than chasing general-purpose intelligence, these companies target specific industries—logistics, manufacturing, healthcare—where immediate value can be realized.

This pragmatic approach is already generating early revenue, giving these firms a potential advantage in sustainability.

The Cost Problem—and the Path to Scale

Despite the excitement, one challenge looms over the entire sector: cost.

Current humanoid robots are expensive to build, often costing tens of thousands of dollars per unit—or more.

This limits adoption to pilot programs and high-value use cases.

To achieve mass-market penetration, companies must dramatically reduce costs while improving performance.

“There’s a parallel here with electric vehicles,” said an industry consultant. “At first, they were expensive and niche. Then scale, supply chains, and innovation brought costs down.”

Key areas of focus include:

- Actuators and motors: Improving efficiency and reducing manufacturing costs

- Battery technology: Extending operational time without increasing weight

- Materials: Balancing durability with affordability

- Supply chains: Achieving economies of scale

Some firms are exploring unconventional approaches, such as simplified designs or hybrid human-robot workflows, to bridge the gap between current capabilities and future ambitions.

The Role of Artificial Intelligence

While hardware challenges are significant, many experts believe the real battleground lies in software.

Advances in AI—particularly in multimodal models—have dramatically expanded what robots can do.

Instead of being programmed step by step, robots can now learn from data, simulations, and real-world experience.

This shift is critical for scalability.

“A robot that needs to be manually programmed for every task will never scale,” said a senior AI researcher. “What you need is a system that can generalize.”

Training these systems, however, is both complex and expensive.

Companies are investing heavily in simulation environments, where robots can learn millions of scenarios without physical risk. Others are collecting real-world data at scale, using fleets of deployed robots to continuously improve performance.

This creates a feedback loop: more robots generate more data, which leads to better models, which in turn improve the robots.

Investors Pour In

The financial stakes are reflected in the surge of investment flowing into the sector.

Over the past two years, venture capital firms, sovereign wealth funds, and corporate investors have collectively committed billions of dollars to humanoid robotics.

Valuations for leading startups have skyrocketed, with some reaching multi-billion-dollar levels despite limited revenue.

“The level of capital is extraordinary,” said one investor. “But so is the risk.”

Unlike software startups, robotics companies face long development cycles, high capital expenditures, and complex manufacturing challenges.

This raises the possibility of consolidation.

“Not everyone will survive,” said the investor. “In fact, most won’t.”

Tech Giants Enter the Arena

Large technology companies are also entering the space, either through internal development or strategic partnerships.

Their advantages are significant:

- Access to vast computational resources

- Established supply chains

- Deep expertise in AI and software

- Global distribution networks

However, they also face challenges, including organizational complexity and slower decision-making processes compared to startups.

“This is a classic innovator’s dilemma,” said an analyst. “Startups are faster, but giants are more powerful.”

China, the U.S., and the Global Divide

The race to build humanoid robots is increasingly shaped by geopolitical dynamics.

China’s manufacturing capabilities and government support give it a strong position in hardware production. The United States, meanwhile, leads in AI research and software development.

Europe and Japan bring strengths in precision engineering and industrial automation.

Rather than a single global winner, some experts predict a fragmented landscape, with different regions dominating different parts of the value chain.

“There may not be one ‘iPhone moment’,” said a strategist. “There could be multiple ecosystems.”

Use Cases: Where the Money Is

While the long-term vision focuses on general-purpose robots, the near-term opportunities are more specific.

Industries currently attracting the most attention include:

- Logistics: Sorting, loading, and last-mile delivery

- Manufacturing: Assembly, inspection, and material handling

- Healthcare: Assistance, rehabilitation, and elder care

- Retail and hospitality: Customer service and operations

These sectors offer clear economic incentives, making them ideal entry points for deployment.

“The key is to find high-value use cases where robots can deliver immediate ROI,” said a business strategist.

Hype vs. Reality

Despite the optimism, some analysts warn of a potential hype cycle.

“The expectations are enormous,” said one market researcher. “But the technology is not yet at the level many people assume.”

Challenges remain in:

- Reliability

- Safety

- Energy efficiency

- Real-world adaptability

If progress falls short of expectations, the industry could face a period of disillusionment—similar to previous waves of AI and robotics development.

However, most experts agree that the long-term trajectory remains intact.

The Platform Question

At the heart of the competition lies a critical question:

Will humanoid robots become a platform?

If so, the implications are profound.

A successful platform could support an entire ecosystem of applications, services, and businesses—much like smartphones did.

This would shift the industry from hardware sales to recurring revenue models, including software subscriptions, updates, and services.

“The real value is not the robot itself,” said a venture capitalist. “It’s what runs on it.”

Conclusion

The race to build humanoid robots is no longer theoretical—it is a full-scale industrial and technological competition.

Billions of dollars are being invested. New companies are emerging. Established players are repositioning themselves.

At stake is not just a new product category, but a potential redefinition of labor, productivity, and human-machine interaction.

Whether humanoid robots become the “next iPhone” remains uncertain.

But one thing is clear:

The companies that get it right will not just build machines—they will shape the future of the global economy.

Discussion about this post